Why is Main Street about to swing back?

I was recently at a cocktail party with some economists, one of those insufferable affairs where people try to sound smart about the economy and the term “K-shape” must have come up fifteen times before the first round hit the table.

It’s the fashionable narrative of the moment.

The “smart money” has decided that the economy is split in two. The top leg of the K goes up (Wall Street, the rich, the people buying Nvidia), and the bottom leg goes down (Main Street, the poor, the people maxing out their credit cards).

The consensus is that this K-shape is permanent. They think we can live in a world where the stock market rips to new highs every day while the average guy gets wrecked by inflation and debt. They think this divergence can last forever.

I have news for you: It can’t.

We are reaching the limits of how far these two realities can stretch before the rubber band snaps. And when it does, the “K” is going to turn into something else entirely.

Anatomy of the K

So what are the features of this “K-shaped” economy? Let’s look at the actual data, because it is pretty wild.

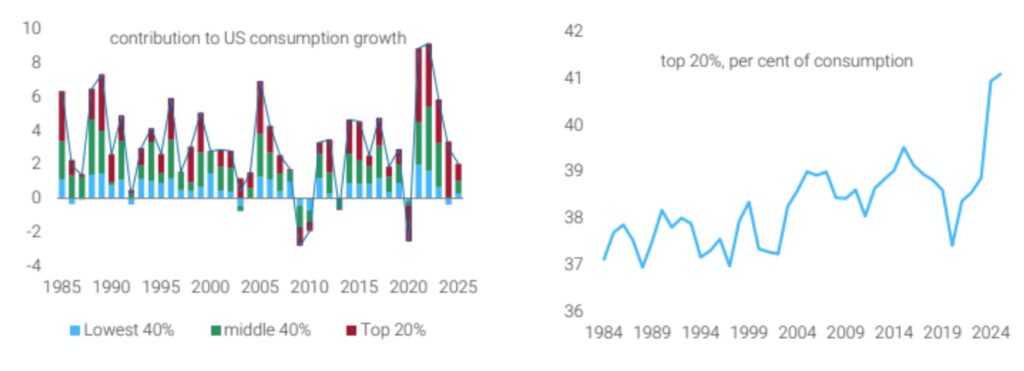

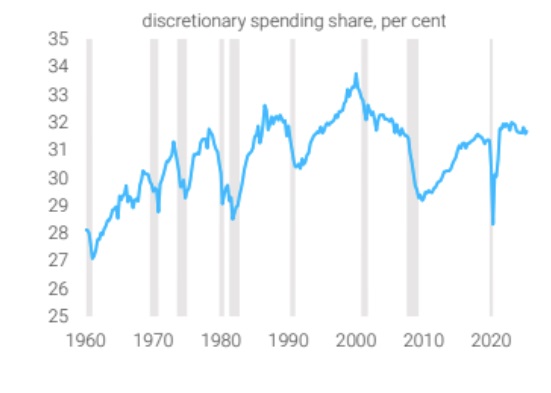

We have a situation where the top 20% of households — the people earning more than $175k a year — have accounted for 85% of US consumption growth since 2023. This is their highest share since at least the early 1980s.

Read that again. 85%.

The top of the food chain is spending like drunken sailors because of the “wealth effect.” Their 401(k)s are up, their houses are up, and they feel rich. Meanwhile, the bottom 40% are totally tapped out. They are defaulting on auto loans and credit cards.

Companies know this. You have Disney basically admitting they are giving up on the middle class to focus on the wealthy. You have Dollar Tree getting crushed while Ralph Lauren is printing money.

But the K-shape isn’t just about households. It’s hitting the corporate world, too.

The market is now dangerously concentrated in just a few superstars. But while the big boys party, the smaller companies are getting absolutely murdered.

More than half of the Russell 2000 is operating at a loss. That is a historical record.

Inequality has been widening for decades, but the gap has blown out in the last two years.

Investors love this “K-shaped” narrative. It’s become their entire worldview.

But let’s be real: It’s mostly just a lazy excuse to stop thinking about macro.

Why did this happen? It wasn’t an accident. It was a combination of five things:

- Immigration:

Remember right after COVID? For a hot minute, the little guy had leverage. Wages at the bottom were ripping because there was nobody to flip the burgers or drive the trucks. It was the only time in recent history we saw actual inequality shrink.

Well, the government fixed that real quick.

They opened the floodgates. We got a massive wave of immigration, which filled all those job openings and crushed wage growth for the working class. It was a classic supply shock. Great for corporate margins, terrible for the guy trying to negotiate a raise at the warehouse.

2. Rates Are Only for the Little People

The Fed hiked rates to 5%, and everyone thought it would slow the economy. It didn’t.

Why? because the superstar companies—the Apples and Microsofts of the world—are sitting on mountains of cash. High rates just mean they earn more interest.

But the bottom of the K? The local dry cleaner? The small manufacturer? They run on floating-rate debt. They are getting absolutely crushed by interest payments. Small businesses are getting strangled while Big Tech is having a champagne toast.

3. The “Wealth Effect” on Steroids

Stocks are up 80% since 2022. That sounds great, right? America is winning!

Except normal people don’t own stocks.

Here is a fun stat: The top 10% of households own 93% of the stock market. The bottom 50% own just 1%.

When housing prices go up, the middle class feels good. When stock prices go up, the rich get richer. And right now, stocks are crushing real estate.

4. Trump’s “Main Street” Betrayal

Trump ran on helping the little guy. But let’s look at the scoreboard.

Tariffs? That’s just a sales tax on poor people who buy stuff at Walmart. The rich don’t care if their imported cheese costs a little more. The poor care if their t-shirts and bananas get more expensive.

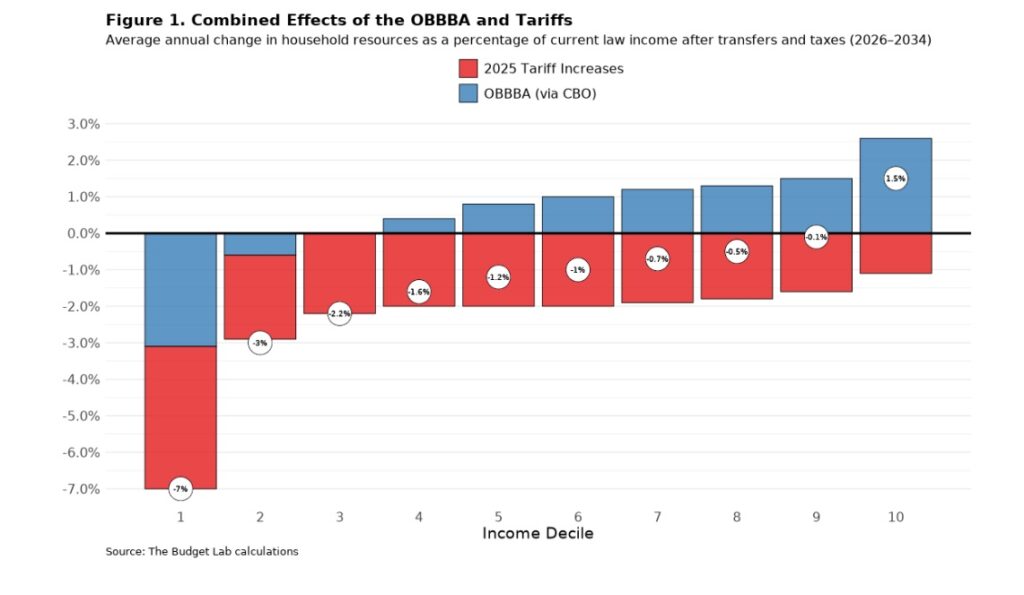

Then you have the budget cuts. Slashing healthcare for low-income earners while cutting taxes for the rich. The Budget Lab ran the numbers: The bottom 10% are taking a 7% income hit. The top 10%? They get a raise.

So much for populism.

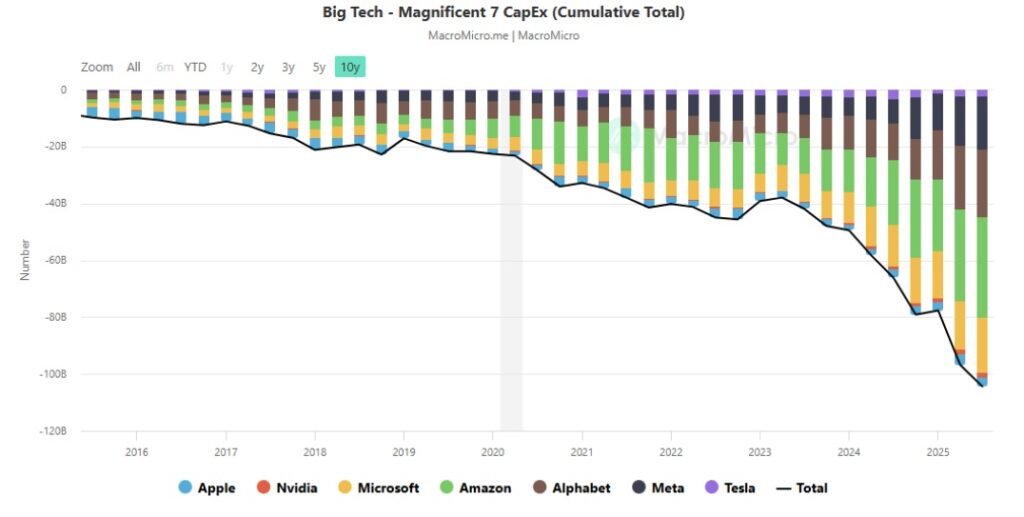

5. The AI Boom

And finally, we have the AI boom. Big Tech is spending $600 billion next year on AI and data centers. That is nearly 2% of GDP just poofed into existence to build the Matrix.

One man’s spending is another man’s income. When Microsoft spends billions, Nvidia books billions in revenue. It’s a giant reflexive loop that pumps the stock market and makes the rich feel invincible.

And the best part? The government exempted GPU imports from tariffs. It’s basically a state-sponsored subsidy for the Mag-7.

The Dangerous Feedback Loop

Put it all together, and you have a market that is building an unsustainable reality. Wall Street is booming, which makes investors feel smart, which makes them buy more stocks, which pushes prices higher. It’s reflexivity 101.

But there is a dangerous arrogance setting in. Investors are starting to say, “The stock market isn’t the economy.” They think it doesn’t matter if Main Street burns down as long as Google keeps buying GPUs.

That is the kind of thinking that gets you carried out on a stretcher.

Big-tech’s resilience

This is what we call recency bias.

Everyone is looking at what happened during COVID. The world ended, but Zoom and Amazon went to the moon. The unemployment rate hit Great Depression levels, and the S&P 500 rallied. So now, the consensus is that Tech is recession-proof .

But you have to understand that technically, there has been only one recession in the past 15 years, COVID was a fake recession.

It wasn’t a real economic cycle. The government printed trillions of dollars and mailed checks to people. Personal incomes actually went up during the fake recession. That has never happened in the history of the world.

A real recession is different. In a real recession, private sector balance sheets get destroyed. People lose their jobs and they don’t get a check from Uncle Sam. They stop buying $1,000 iPhones. They cancel their Netflix.

In a normal recession, two things happen:

- Multiples Crush: Risk premia widen. PE ratios collapse.

- Earnings Crush: Every recession in history has reduced corporate earnings by 10–30%.

The bulls think the Mag-7 are immune to this. They think these companies are utilities.

They are not utilities.

Look at the revenue mix. In 2024, roughly half of Big Tech’s revenue came from “monetizing eyeballs” (ads) and the other half from infrastructure.

Investors are forgetting that the “Mag-7” stocks are not magical utility companies. They rely heavily on advertising and discretionary consumption.

Alphabet and Meta are ad companies. Amazon sells stuff to consumers. Apple sells luxury tech.

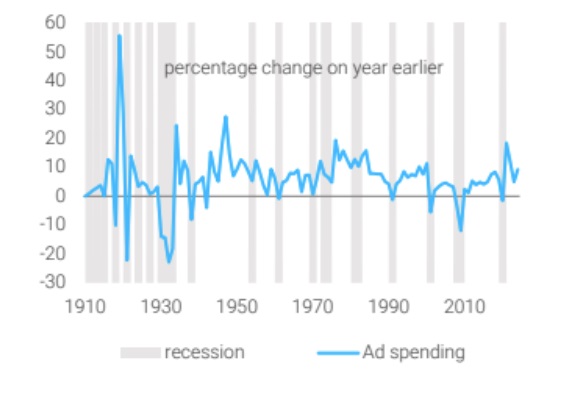

Advertising spending is notoriously cyclical. When the economy rolls over, the first thing companies cut is their ad budget.

But hey, what about the data centers and all of this AI Capex spending – is this spending recession-proof?

The bull case is that Big Tech will keep spending billions on Nvidia chips regardless of the economy because they are in an arms race.

Right now, the momentum is insane. We are seeing blatant CapEx recycling and vendor financing—Nvidia is literally offering loans to customers so they can buy more GPUs. That is never a good sign.

But here is the scary number: Current CapEx levels are running at 60% of Big Tech’s earnings. This is a 75% YoY growth.

That is not far off from what we saw during the Dotcom bubble.

If we get a slowdown, and revenue disappoints, do you really think Zuck and Nadella are going to keep lighting cash on fire at this rate?

And here is the kicker: We don’t even need a contraction. We just need a slowdown.

If the Mag-7 companies merely spend the same amount in 2026 as they did in 2025—zero growth—Nvidia’s earnings are going to disappoint.

And then the whole trade unravels.

Never forget: Semiconductors are the most cyclical form of capex demand.

Main Street catches up

So the question is: Is this “K-shaped” economy sustainable?

The consensus says yes. They think this is the new Goldilocks. The macro environment is “just right”—too cold for inflation, but hot enough for the Mag-7 to keep ripping.

But the cynic in me (and let’s be honest, I am a professional cynic) thinks the “K-shape” narrative is just a lazy excuse not to think about macro at all.

It’s an intellectual cop-out. It allows investors to ignore the business cycle because “Big Tech is different.”

But trees don’t grow to the sky. We are looking at three scenarios for 2026, and only one of them makes sense to me.

The Three Doors

- The Melt-Up (Status Quo): The K-shape continues. The AI bubble gets bigger because bull markets love a simple story. This is fun for a while, until it isn’t. Bubbles burst. Wealth gets destroyed.

- The Nuke (Recession): The labor market faces disruption. Employment decreases, confidence diminishes, and consumer spending on high-value electronics declines. Advertising expenditure collapses. The capital expenditure boom in Artificial Intelligence concludes. Big Tech is not impervious to these pressures.

- The Rebound: The economy recovers. Hiring picks up. Pent-up demand gets unleashed. Basically the lower line of the K-shape plays catch up with the upper line.

I am betting on Door #3.

Fiscal policy is turning reflationary. Monetary policy and balance sheet policy are loosening. We are going to see GDP upgrades for 2026.

But here is the catch: Inflation.

If the economy rips, inflation comes back. And that means the Fed might have to hike rates. Or, if the Fed tries to be cute and keep rates low (maybe because Trump appoints a dove), the bond market will do the tightening for them.

Bubbles don’t usually die of old age. The Fed murders them.

The End of Neoliberalism

Trump ran on helping Main Street. Ironically, his tax cuts helped Wall Street. But the long-term impact of his policies – tariffs and immigration – is going to shift the balance of power.

Here is the reality:

- Running it Hot: Trump loves debt. Deficits are going to stay high. That creates a high-pressure labor market.

- Immigration: Restricting immigration creates labor mismatches. It reduces supply more than demand. That is inflationary. It pushes wages up.

- Tariffs: Tariffs are basically deglobalization. We are unwinding 50 years of shipping jobs to the lowest bidder.

For the last 40 years, Capital beat Labor. Wall Street beat Main Street. Neoliberalism crushed worker power.

That era is over. The pendulum is swinging back.

We are facing secular labor shortages. Demographics are destiny. Just look at Japan if you want to see our future.

When labor is scarce, labor gets paid.

The AI Head-Fake

But Hoang, Sam Altman says AI is going to take all our jobs and we’ll all be living on UBI.

I don’t buy it.

I think the capabilities of AI are being massively overhyped.

Technology is usually labor-augmenting, not labor-replacing. It makes workers more productive, which allows them to capture a share of the gains.

I’m with David Autor on this one. AI lifts up the middle class. It helps the mid-curve worker perform like a top-tier worker. It doesn’t hollow out the middle; it restores it.

If you are betting on mass unemployment and a permanent capital-friendly environment, you might step on the wrong side of the trade.

The Bottom Line – Betting against the K

The “K-shaped” economy is on borrowed time.

It’s currently “too cold” at the bottom leg and “too hot” at the top one. But that equilibrium is fragile.

If we get the reflationary re-acceleration that I expect, Main Street is going to have a great 2026. Wages will rise. The little guy will catch a break.

But Wall Street?

That’s a different story.

A booming economy with capacity constraints means inflation. And inflation is the kryptonite for high-duration tech stocks.

The Fed is cutting rates now, but the bond vigilantes are watching.

Don’t get complacent. The pendulum is moving.